DocuSign

$DOCU

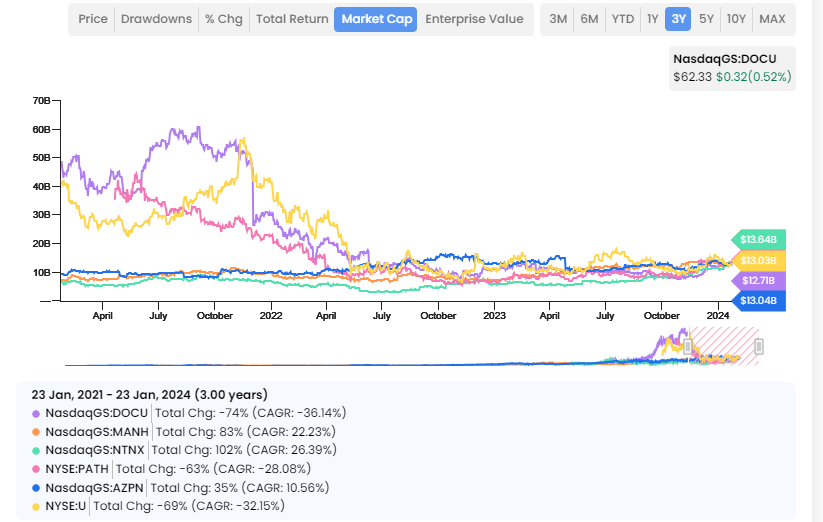

DOCU 0.00%↑ is one of the COVID names that I don’t hear too much about anymore. The chart below shows the rerating of valuations that’s taken place over the past few years. Things appear to have leveled off, and are gradually, and perhaps more rationally appreciating.

The $20 billion(ish) market cap range appears to be the apex of what this current market regime will tolerate. It represents a growth prop from DOCU 0.00%↑ current market cap, if you believe it to be achievable.

It also coincides with around the area that the AVWAP from the company’s IPO falls. This is the average cost basis for investors who hypothetically bought since the IPO. Balanced against prior low points offers an almost 2:1 risk prop.

The stock made a nice move through its 200 day following its December earnings report, and continued consolidation above that level as evidenced below furthers the attraction on the long side.